In recent years, the phrase Forex Indonesia has come to represent more than just a place to exchange currency. It now reflects a dual movement — one driven by fintech and trading platforms offering digital currency speculation, and the other by the enduring presence of traditional money changers that cater to daily, practical needs. Both are growing, but they’re growing apart in function, purpose, and user behavior.

This split reflects broader economic trends: increased digitization, growing personal financial interest, and a maturing financial literacy rate among Indonesians. But it also highlights a core question — which service is best for which need?

Forex Indonesia: Digital Trading Gains Ground Among the Curious and the Brave

Forex trading platforms have been gaining visibility in Indonesia, especially among Gen Z and millennial audiences who are more comfortable with mobile apps, online dashboards, and real-time analytics. In this model, traders don’t physically exchange cash. Instead, they speculate on currency pair price movements — say, between the rupiah and the US dollar — hoping to profit as rates shift.

These platforms typically operate 24/5 and are supported by licensed brokers regulated by BAPPEBTI (Indonesia’s Commodity Futures Trading Regulatory Agency). The appeal is clear: flexible access, potential for high returns, and the excitement of participating in a global market. But this also comes with volatility. Unlike a simple cash exchange, forex trading involves leverage, technical indicators, and constant decision-making.

The rise in online education, trading communities, and demo apps has made forex trading more approachable. Yet it still requires users to actively manage risk, understand global economic triggers, and have the emotional discipline to navigate losses.

Forex Indonesia: Meanwhile, Money Changers Hold Their Ground in Daily Life

Source: The Conversation

Despite the digital surge, traditional money changers remain firmly planted in Indonesian cities — particularly in tourist zones, shopping areas, and business districts. These brick-and-mortar services offer something online platforms do not: physical currency, exchanged in-person, with clarity and immediacy.

Whether someone is traveling abroad, paying school fees overseas, or receiving remittances, money changers still serve a crucial role. Regulated by Bank Indonesia, these outlets provide rates based on market movements, adjusted with a fixed margin for profit. The experience is fast, familiar, and human — and for many, that still holds value.

Interestingly, in smaller cities and among older generations, money changers are not just financial outlets but community fixtures — often known by name, trusted for decades, and recommended by word of mouth. Their relevance in the Forex Indonesia environment hasn’t diminished; it’s simply become more specialized.

Forex Indonesia: One Term, Two Worlds: Understanding the Functional Gap

Source: The European Business Review

The phrase “Forex Indonesia” might imply a single industry, but in reality, it refers to two very different ecosystems. On one side is the high-speed, speculative, and digital space of forex trading. On the other is the steady, service-oriented environment of money exchange counters.

Each appeals to different needs. Forex trading is aspirational — it invites users to learn, risk, and engage with a fast-paced market. Money changers are transactional — they provide straightforward utility without requiring users to predict price movements or monitor global trends. The divide isn’t about which is better, but rather, about purpose.

Consumer Behavior Is Evolving — But Not Uniformly

Source: Niaga.asia

Indonesia’s growing financial inclusion has given rise to different levels of user readiness. Urban millennials may be eager to try forex trading apps with a few taps, while rural users or older clients might stick to familiar cash counters. Trust and transparency also play a role — many still feel more confident seeing actual money exchanged in hand than interacting with abstract graphs on a screen.

Even so, consumer education is slowly narrowing this gap. BAPPEBTI has made efforts to regulate platforms and raise awareness around legitimate brokers. At the same time, Bank Indonesia continues to tighten oversight on licensed money changers to ensure fair pricing and consumer protection. These dual efforts are helping maintain trust in both sides of the Forex Indonesia space.

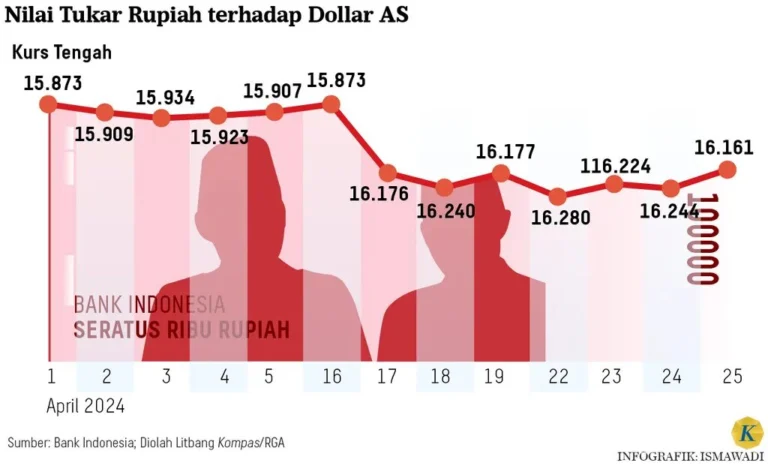

Pricing: A Tale of Transparency and Timing

Source: Kompas

While both services revolve around currency value, their pricing mechanisms differ. Forex platforms display live interbank rates, often offering competitive spreads and commission-based structures. These prices shift by the second and allow for split-second decisions — ideal for traders.

Money changers, by contrast, operate with posted daily rates, often including a margin that covers operational costs. The pricing is stable and predictable — helpful for consumers who need clarity and control, not market exposure. This divergence reflects the differing needs of users: traders want opportunity; customers want certainty.

Regulation and Legitimacy Remain Central to Trust

Source: Banksinarmas

One common factor that bridges both models is the importance of regulation. In a space where scams and unlicensed operators are still an issue, the roles of BAPPEBTI and Bank Indonesia are critical. Traders are urged to verify their brokers on BAPPEBTI’s official list, while customers should check for proper licensing before exchanging money.

This emphasis on legality is reshaping how Indonesians view forex services. There’s growing awareness that “easy money” rarely ends well without safeguards. Within the Forex Indonesia market, legitimacy is becoming as important as access — and that’s a healthy shift.

Looking Ahead: Two Roads, Same Destination?

So where is Forex Indonesia heading? Likely, toward greater differentiation and coexistence. As digital trading continues to attract younger users and fintech partnerships, traditional money changers will stay relevant by focusing on service reliability and physical access. Both will remain integral — not just as financial tools, but as reflections of how Indonesians engage with money itself.

The real takeaway isn’t choosing one over the other, but understanding what each offers — and when. Because in a country as dynamic as Indonesia, financial behavior isn’t just about trends. It’s about trust, access, and purpose.